Calm after the chaos

11932 Arbor Street, Suite 103, Omaha, NE 68144

Calm after the chaos

11932 Arbor Street, Suite 103, Omaha, NE 68144

We help commercial property owners restore damaged property quickly so that their businesses, tenants, and stakeholders can get back to business as quickly as possible.

About every roofing contractor you encounter claims to be "experts" at handling insurance claims, but could that be true? It's an easy claim to make, but few have the actual education, experience, or expertise worthy of such a claim. When it comes to storm damage restoration, not all contractors are created equal-and that's where we stand out from the crowd. Our team brings a level of education and training that sets a higher standard in the industry. While many competitors rely on basic on-the-job experience, our professionals hold advanced certifications from organizations like the Institute of Inspection, Cleaning and Restoration Certification (IICRC) and have completed rigorous coursework from organizations like HAAG Engineering.

But why are these things so important to you? Because after a covered loss you need a professional to help identify all elements of damage, a person with the knowledge to help get carrier approval, and a company with the resources to perform all that work. Beyond education, our expertise is honed by years of specialized experience that many competitors simply can't match. We've tackled everything from minor roof leaks to catastrophic hurricane aftermaths, giving us a nuanced understanding of how storms uniquely impact different homes and what damage we need to look out for. Unlike some contractors who offer a one-size-fits-all approach or only do certain trades like roofing or siding, we customize every restoration plan and leverage cutting-edge tools like thermal imaging and moisture mapping to pinpoint hidden damage others might miss. Our team stays ahead of industry trends, regularly training with the latest techniques and equipment, so you're not just getting a quick patch-up. You're getting a comprehensive restoration that protects your home's value and your peace of mind. When you choose us, you're choosing a contractor that combines academic precision with real-world mastery, delivering results that outshine the competition.

We've been around for more than a decade as an A+ Rated BBB business

All trade crews are certified in their respective field and every insurance claim is reviewed by a licensed attorney

Insurance claims are billed per scope, ensuring you never have any out-of-pocket expense beyond your deductible

We offer a Lifetime Warranty on our workmanship

If you've never been through a storm damage claim, it can feel overwhelming. Worst of all, any time a process is unclear or confusing, there is an opportunity for bad actors to take advantage of you. We approach the insurance claim process as an opportunity to educate and inform our customers about the claims process, the various terms you'll encounter, and even how the insurance proceeds are handled. Once we feel you have a good understanding of the process, we will ask if we can do the work for you - and that is as "pushy" as we will get!

After a storm, such as wind or hail, do you have damage to your property? While it might be tempting to simply look up at your roof or walk around your house, you should get a trained professional to actually inspect things like your roof, siding, gutters, windows, and other elements that are commonly damaged by weather. Some storms and some damage may be so obvious that a trained professional isn't needed - at least initially. But any time there is a potential loss it should be inspected, and not just by anybody - make sure it is a trained professional with actual experience and education. Most storm contractors will offer free initial inspections. Here are some things to consider for this initial inspection:

Choose a company with trained inspectors - not just sales people. Ask if the inspectors have any certifications or licenses (but licensure for this inspection isn't required in Nebraska). JRS inspectors either hold these certification & licenses, or were trained or overseen by those who do.

We can't stress this enough - if the "inspector" just comes off the roof and says "there is damage" or "there is no damage" - run the other way. Only deal with inspectors who will provide you documentation of what they found. JRS inspectors create and provide an annotated photo report of any property we physically step foot on - giving you real date & time stamped evidence of what was found.

While this aspect may seem more fit as a dating tip, how the inspector is dressed or how friendly they are can indicate what type of people the company hires. Storm claims deal with big, important issues - often with large sums of money involved. If the inspector is dressed shabby or otherwise appears shady, it's probably a good indication that the company he or she works for is shady too. One of JRS's key hiring requirements is presentability, because we know that we are trying to earn your trust & confidence at every step.

If there is damage that warrants a claim, you simply need to open the claim by calling the claims office of your insurer. You can also call your agent, who can facilitate opening a claim under your policy. Some insurers even provide apps and online forms to start a claim. Once the claim in opened, your insurer will usually send out an adjuster to physically inspect your property. Some insurers have been using drones to do virtual inspections; some insurers have relied on the contractor to provide a walk-through, real-time virtual inspection via an app; and we've even seen some insurers accept JRS's proposed scopes of loss and photos. But however the insurer verifies your claim, it is best to have JRS representatives involved, either by physically meeting the adjusters on site or being involved in the virtual inspection. We have provided links to the online claim departments of some major insurers that we work with:

The above list is not exhaustive - JRS works with any P&C insurance provider. If your insurer's claim department is not listed above, either google the name of your insurer's claims department or call your agent.

Once the insurer approves your claim they will send you a document outlining what they have approved. Some homeowners and agents call this an estimate, but we refer to this as the "Scope of Loss." Insurers use software vendors to adjust claims. The most common software is Xactimate, which is made by Verisk. These software vendors publish pricing for anything from landscaping lights and insulation all the way to roofing materials & labor. The idea is that by using Xactimate pricing the insurers know the fair market value of all items contained in a claim. JRS and other storm contractors license this same software, so we already know what insurers are paying for every type of item in every market across the country. However, the problem is that these claims are scoped out by adjusters, not contractors. Many times the adjusters may not account for necessary or consequential items. More often than not, initial scopes are underwritten - leaving the insured with a risk of out-of-pocket expenses or without necessary work that is required to bring the home to its pre-loss condition. That is why it is paramount to work with an experienced storm damage contractor - a company with the knowledge, experience, & dedication to ensuring you obtain full indemnity under your policy.

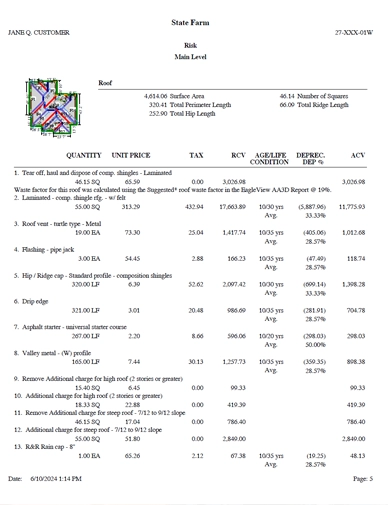

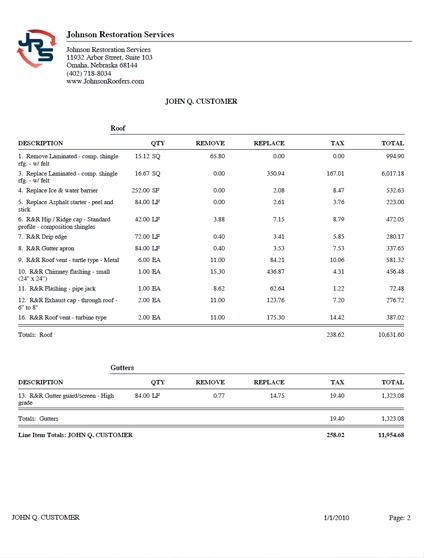

While some details may differ between carriers, such as headings, cover pages, and logos, the general structure, format, and content will look like the samples shown here.

Our staff is certified in writing Xactimate Scopes & trained in submitting supplements.

JRS provides you copies of photo reports, supplement requests, and insurer communications.

JRS does not ask for deposits or pre-payments. You only pay after work is completed and inspected by you.

Sample Scope Docs

Sample Scope Docs

It may or may not come as a surprise, but insurers often underwrite claims. They may leave off necessary components - even those required by the building code - or they may not include elements of damage that go unnoticed or are never brought to your attention. Whatever the reasons, it is vitally important to have a qualified and experienced contractor look over your scope of loss and ensure you are getting full indemnity under the claim. The bottom line is that you should not have any out-of-pocket expense beyond your deductible (unless you have opted for less than full coverage under your policy).

Once you receive your scope of loss document from your insurer, JRS representatives will sit down and go through it line by line, noting any deficiencies or errors. Once we have a good understanding of all elements of damage and what is necessary to bring your property to its pre-loss condition, we scope out the claim in Xactimate and submit it to your insurer for approval. This process is called "supplementing" the claim. JRS provides your insurer with citations to the building code, photos of missing or overlooked damage, as well as other supporting documents.

Some aspects of your claim can be completed right away, without waiting for supplement approvals. However, if certain items were missing, the insurer may want to reinspect the property to ensure the supplements are valid. But as items get approved by your insurer JRS will begin scheduling the work. Once all items are completed, JRS will submit final documentation - called a "Statement of Work" - to your insurer and any remaining insurance proceeds will be released.

Did we do a good job? Were we responsive? Did we get you full indemnity? If you were satisfied with how JRS handled your claim, the best compliment you can give is by referring your friends, family, and others. More than 90% of our customers come from referrals!

If your car gets totaled, your insurer doesn't buy you a brand new car, right? However, most homeowners policies have Replacement Cost Coverage - meaning that even if your roof or siding is 20 years old, the policy is liable to pay for brand new, replacement items. The total cost to replace given items is called the Replacement Cost Value, or the "RCV".

The Actual Cash Value, or "ACV", is synonymous with "fair market value." That is, the ACV represents the total Replacement Cost Value, less its depreciation based on its age and condition. For example, if a roof has a 20 year useful life and it is 10 years old, the RCV for the roof would be depreciated or reduced by 50%.

Regardless of what supplements ultimately do or do not get approved, all insurance proceeds will be issued to you, the insured. JRS does not direct-bill any insurers and normally JRS will not be listed as a payee on insurance checks. However, sometimes mortgage companies may be co-payees, in which case the mortgage company may require that the contractor who does work and provides lien waivers be listed as a co-payee when the mortgage company re-issues insurance claim checks.

No! Unless you have opted and purchased a policy that doesn't have full coverage, any storm-related work should be covered under your policy. JRS is extremely knowledgable and tenacious when it comes to helping obtain full indemnity for our customers, so unless something is specifically excluded in your policy or you ask for additional work outside of storm damage repairs, you will never be responsible for anything beyond your deductible.

No. Some agents or adjusters may tell you to get 3 bids, and that may be considered standard practice when getting most cash or bid-based construction work done, but you are not obligated under your policy to do so. More importantly, in a cash/bid project scenario, the customer says something like "please give me a bid to build me a deck." But when we are talking about storm damage repairs we first need to know what damage is being covered under the policy. So if you want to get 3 bids, you still need to have your insurer tell you what is being covered and then you can ask contractors to give you bids for those items.

Yes. This is the document that outlines what is being covered by your insurer. First, you want a qualified and experienced contractor like JRS to look it over and let you know if anything is missing (which is often the case). Second, your contractor needs to know what work you want done or what work is being paid for by insurance. The only way to ensure you aren't going to be stuck with out-of-pocket expenses is to make sure all the work being done is going to be covered by your insurance policy. Third, while some customers may think the insurance document contains some secret information, it doesn't. JRS and most other storm contractors license the exact same software that the insurance company uses to adjust claims. That is, we already know what the insurer pays for various items - this is not hidden and not secret. Lastly, even if a contractor is willing to do the work for less money than is indicated on the insurance paperwork, the insurer will only release that amount of recoverable depreciation that you actually spend. In other words, getting a cheaper contractor doesn't put money in your pocket, it just saves a few bucks for your insurance company.

When disaster strikes, JRS brings calm after the chaos by timely planning and implementing a mitigation plan, managing the claims process, and restoring your property to its pre-loss condition.